The situation described as a “liquidity trap is an ever more relevant economic concept today, with many European economies and the United States struggling with low inflation rates or even deflation accompanied with low economic growth and very low to even negative base interest rates.

Growth and Deflation

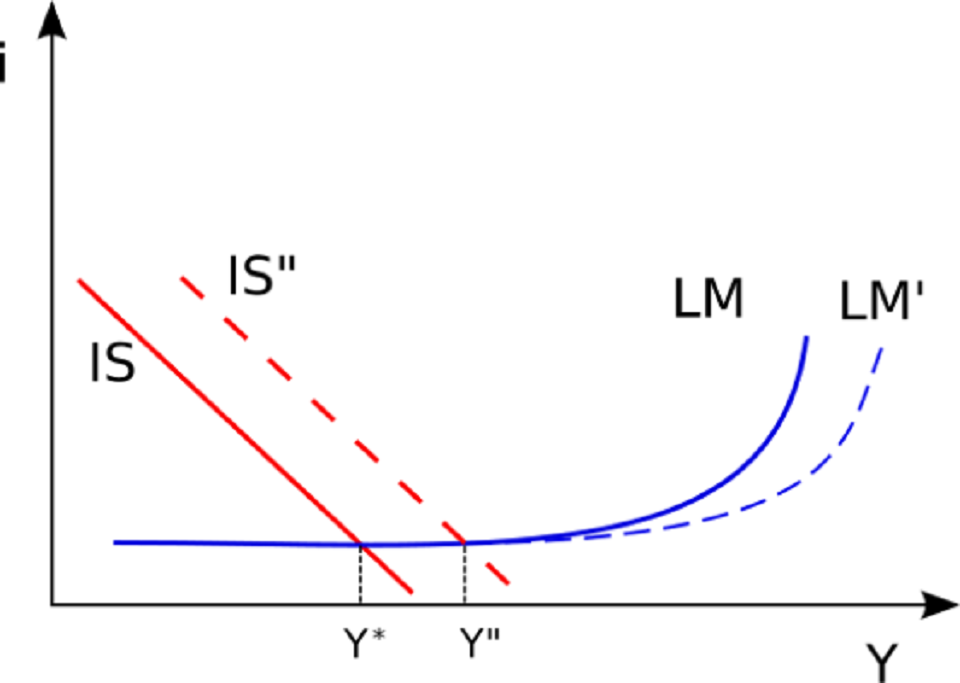

When conventional monetary policies have become impotent and nominal interest rates are at or near zero with no effect; we have what economists call a liquidity trap.

This was true in Japan during the 1990s and the United States in the 1930s. When interest rates had reached very low levels but with little to no effect on economic inflation or growth. U.S. interest rates were close to zero during the second half of the 1930s and the same was true in Japan during the second half of the 1990s. In 1999 the Japanese short-term interest rates were only 0,1 percent.

Expansionary monetary policy relies on the logic of when reducing interest rates, this would stimulate investment spendings. But when interest rates are at a very low level already, close to zero, then any further aggressive monetary policy would be less effective, naturally. Making it difficult for central banks to have any impact on monetary policy, a situation that several economies are facing today, again.

As expansionary monetary policy raises the supply of money, this raising liquidity levels, but since interest rates cannot fall any further, this liquidity has no effect – thereby aggregate demand, production, and employment are “trapped” at low levels.

In the Wake of Financial Crisis

After the financial collapse of 2007, the United States and Europe faced short-term policy rates close to zero. The U.S. Central Bank, The Federal Reserve (FED), responded to the financial crisis to stabilize the economy and the financial system. They reduced the level of short-term interest rates to near zero and also longer-term interest rates.

The FED also began purchasing large quantities of longer-term Treasury securities and longer-term securities issued or guaranteed by agencies such as Fannie Mae or Freddie Mac.

A situation emerged that looked very much like a liquidity trap and some economists, among those Paul Krugman who has studied the economics of the Great Depression meticulously, argued and warned repeatedly that the U.S. was heading in the direction of a dangerous liquidity trap.

Indeed, a tripling of the U.S. monetary base between 2008 and 2011 failed to produce any significant effect on U.S. domestic price indices.

The situation in the U.S. today still resembles a liquidity trap. Since at present time the FED interest rates are very close to zero with a very low inflation rate (1 percent in January 2014).

This is also true for several other countries in Europe. And Japan is still one of those struggling with very low inflation levels, despite the many attempts by the Bank of Japan to stimulate the economy. Inflation levels for the Japanese economy have remained around zero for long periods, with little effect on inflation, with even intermediate deflation.

Deflation was true for some periods during 2013 but the inflation rate has recently begun to accelerate – probably due to the recently elected Prime Minister Shinzo Abe’s campaign aiming to end two decades of low economic growth and stagnation. It remains to be seen if the economic policies implemented by Abe, called ‘Abenomics’, will be successful in the long run.

How to Escape the Trap?

In economics, the rationale is that expectations affect behavior and thereby real economic factors in the economy. Nominal rates are confined to the zero level, but not real rates. And since expansionary monetary policy might raise inflation expectation, the mere fact that announced stimulus, could lower real interest rates below zero and thereby stimulate the economy and raise investment spending.

Another response to monetary expansion is that of causing deliberate currency depreciation and making the nation’s goods cheaper and more attractive abroad – thereby increasing exports, raising incomes and stimulating the economy.

In the wake of the financial crises, many central banks have responded to the situation with a somewhat unconventional monetary policy called quantitative easing, in which to stimulate the economy, the banks start buying specified amounts of financial assets from commercial banks and other private institutions. Thereby increasing the monetary base on those financial assets. It is an experiment and remains unclear at the moment, if this will, in fact, have any effect on the economy.

_______________

Inflation United States – consumer price index (CPI)

FED Federal Funds Rate, American central bank’s interest rate

______________________________